New D.C. Circuit Case Underscores When Tax Whistleblowers Should Consider Appealing to Court

The U.S. Court of Appeals for the D.C. Circuit (which hears all appeals from U.S. Tax Court cases involving whistleblowers)...

The U.S. Court of Appeals for the D.C. Circuit (which hears all appeals from U.S. Tax Court cases involving whistleblowers)...

Congress allocated a total of $669 billion to the Small Business Association (SBA) and the Paycheck Protection Program (PPP) so...

The mandatory tax whistleblower program has been a boon for the U.S. government, bringing in more than $616 million in...

The IRS just released its annual report on the whistleblower program – showing over $616 million dollars brought into the Treasury...

A guest post from Dean Zerbe, senior policy analyst for the National Whistleblower Center and former tax counsel for the Senate...

A guest post from Dean Zerbe, senior policy analyst for the National Whistleblower Center and former tax counsel for the Senate...

The NWC releases today an extensive commentary that was written by myself and Steve Kohn (with a huge assist from...

By Dean Zerbe, Advisor to NWC and Attorney at Zerbe, Fingeret, Frank & Jadav. Dean Zerbe Tax Court in a...

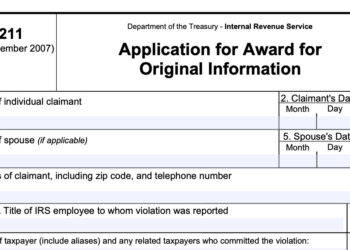

If You Get A Rejection Letter From The IRS

Whistleblower Network News is an independent online newspaper providing our readers with up-to-date information on whistleblowing. Our goal is to be the best source of information on important qui tam, anti-corruption, compliance, and whistleblower law developments.

Copyright © 2021, Whistleblower Network News. All Rights Reserved.

This Newspaper/Web Site is made available by the publisher for educational purposes only as well as to give you general information and a general understanding of the law, not to provide specific legal advice. By using this website, you understand that there is no attorney-client relationship between you and the Newspaper/Web Site publisher. The Newspaper/Web Site should not be used as a substitute for competent legal advice from a licensed professional attorney in your state.